")

mihailomilovanovic/E+ by way of Getty Pictures

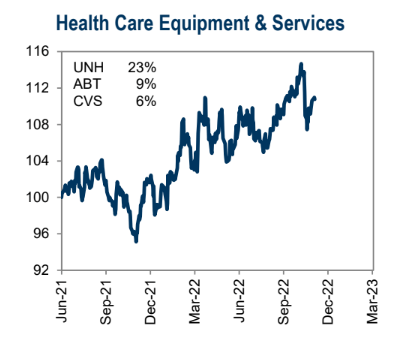

Well being Care provides shares have normally been in want during the last yr. The crowd, led by way of UnitedHealthcare (UNH), Abbott Laboratories (ABT), and CVS (CVS) has trended up towards the extensive marketplace. However it is a numerous staff with many smaller gamers in riskier niches. One home identify was once an surprising pandemic winner, however now faces govt shifts on the most sensible at the side of suffering bottom-line income.

Well being Care Apparatus Names With Relative Power

Goldman Sachs Funding Analysis

In keeping with Financial institution of The united states International Analysis, Dentsply Sirona (NASDAQ:XRAY) is without doubt one of the international’s biggest dental producers, offering dental places of work with general answers starting from consumables to high-end apparatus. The corporate has operations in over 120 nations. It operates thru two segments, Applied sciences & Apparatus, and Consumables.

The North Carolina-based $6.5 billion marketplace cap Well being Care Apparatus & Provides business corporate inside the Well being Care sector has detrimental GAAP profits over the last three hundred and sixty five days and will pay a 1.7% dividend yield, in step with The Wall Boulevard Magazine.

Stocks have been at the transfer upper in mid-November when some activist investor chatter made the rounds, however the ones positive aspects proved brief inside a broader downtrend. Additionally taking place right through the center of ultimate month was once a very powerful EPS omit in XRAY’s Q3 record. The company additionally fell brief on income forecasts.

Dentsply Sirona has a risky profits historical past with its huge multinational presence. There are headwinds from macro problems like FX at the side of uncertainty surrounding contemporary CEO and CFO adjustments. Nonetheless, there may be some cushion observed in its reasonably solid portfolio of dental production actions. Drawback dangers come with a slowdown in international expansion and imaginable lagging apparatus gross sales following Covid. Upside possible stems from certain gross sales tasks after the release of Primescan and different merchandise.

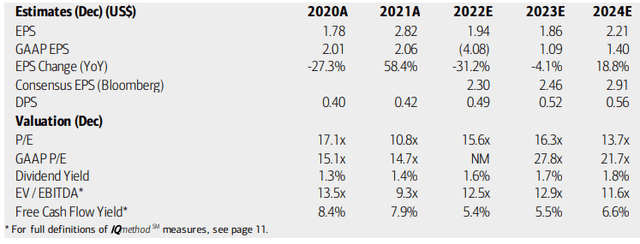

On valuation, analysts at BofA see profits having fallen sharply this yr and losing once more in 2023, regardless that at a extra modest fee. The Bloomberg consensus forecast is extra upbeat on each general running profits in line with percentage and the expansion trajectory. Dividends in the meantime are anticipated to upward push, regardless that the yield will keep underneath 2% it seems that.

XRAY has a near-market ahead non-GAAP P/E whilst its GAAP P/E is way upper the usage of ahead estimates. The excellent news is that the company is unfastened money float certain, however the EV/EBITDA more than one isn’t in particular horny given unsure expansion. Total, I’m really not satisfied this can be a cast worth tale presently.

Dentsply Sirona: Income, Valuation, Loose Money Drift Forecasts

Stockcharts.com

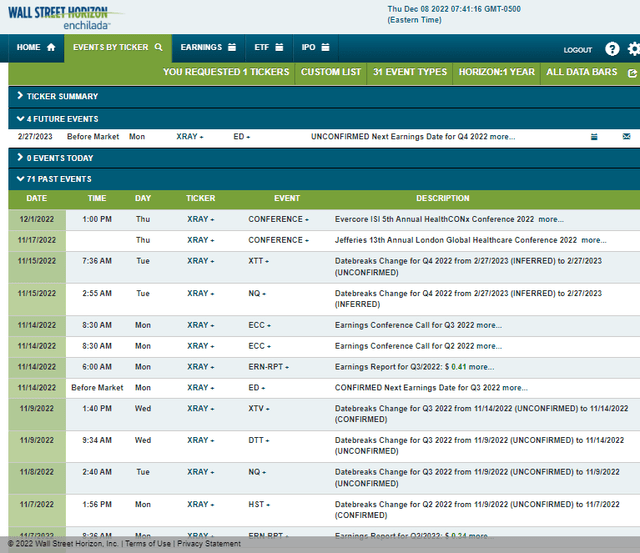

Taking a look forward, company tournament knowledge from Wall Boulevard Horizon display an unconfirmed Q3 2022 profits date of Monday, February 27 earlier than marketplace open. The company not too long ago spoke at a couple of meetings, however the ones occasions didn’t do a lot to lend a hand the inventory worth.

Company Match Calendar

Wall Boulevard Horizon

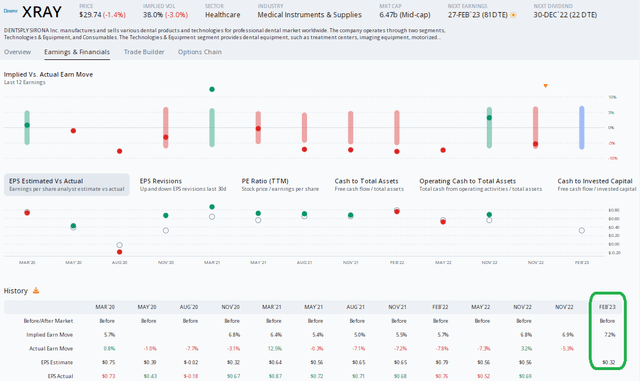

Digging into the impending profits record, knowledge from Choice Analysis & Era Services and products (ORATS) presentations an anticipated per-share benefit determine of $0.32 which might be a pointy decline from $0.76 of EPS observed in the similar quarter a yr in the past. Implied volatility isn’t exceptionally excessive presently, close to 38%, so don’t be expecting large strikes within the inventory worth any time quickly.

Income Enlargement Anticipated to be Unfavorable YoY

ORATS

The Technical Take

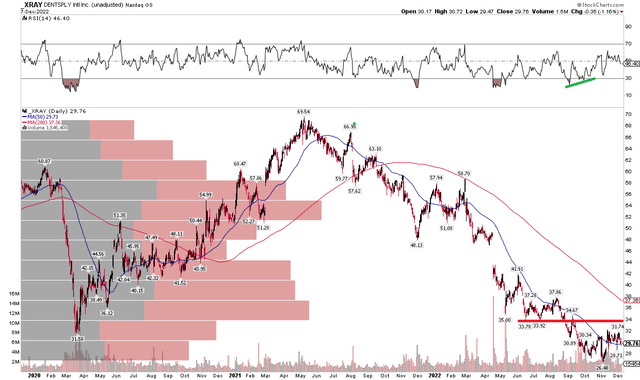

XRAY was once a large winner popping out of the pandemic with the inventory emerging from close to $30 to just about $70 by way of Q2 2021. The ultimate year-and-a-half has been a downward trip, regardless that. I see some imaginable indicators of a slowdown in bearish momentum, as evidenced by way of an progressed RSI on the most sensible of the chart, however with a pronounced downtrend in position and resistance close to $32 and $34, at the side of a downward-sloping 200-day shifting reasonable, the rage is just too arduous to battle in this well being care identify.

XRAY: A Protracted Downtrend

Stockcharts.com

The Backside Line

XRAY’s unsure profits outlook, lukewarm valuation, and bearish worth development make me a dealer presently. We want to see proof of higher running effects at the side of a reversal at the chart.